Secure Your Emergency Fund: Avoid These 3 Cash Storage Mistakes at Home

Emergency cash at home is only helpful if it’s still there—and still usable—when you need it. This article shows how to secure your emergency fund by avoiding three common at-home cash storage mistakes: relying on obvious hiding spots, failing to protect bills from fire and water damage, and treating home cash as your entire emergency plan instead of a limited, accessible layer. You’ll get practical storage upgrades, a simple split between home cash and safer reserves, plus guidance that supports smarter spending, budgeting, and basic credit-file awareness.

Keeping some emergency cash at home can bring real peace of mind—until it’s misplaced, damaged, or too easy for someone else to find. If your goal is to secure your emergency fund, these three common at-home storage mistakes are the ones to fix first, with practical alternatives that still keep cash accessible.

Mistake 1: Storing Cash In Obvious “Hiding Spots”

Nightstands, sock drawers, cookie jars, and under-mattress stashes are the first places most thieves (and even curious visitors) check. They’re also the places you’re most likely to forget when life gets hectic, which matters when you’re deciding where to keep large amount of money temporarily.

A better approach is to treat cash storage like layers: keep a small “grab-and-go” amount in a discreet spot, and store the rest in a more secure container. If you’re wondering about the safest place to put money at home, it’s rarely a hiding spot—it’s a protective system.

What To Do Instead

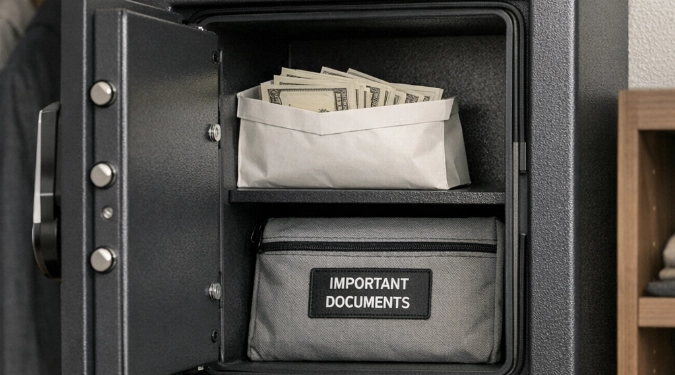

- Use a fire-rated, theft-resistant safe that can be bolted to a floor joist or wall stud.

- Choose a location that’s not the primary bedroom; obvious rooms are searched first.

- Limit who knows the safe exists, and avoid sharing combinations or keys casually.

Mistake 2: Skipping Protection From Fire, Water, And Routine Wear

Cash is paper—so the biggest threat is often the ordinary: house fires, burst pipes, humidity, or even a spill. People often wrap bills in plastic and assume they’re protected, but heat can still destroy them and moisture can still cause damage over time.

If you ever conduct a home risk assessment and realize a weakness in how valuables are protected, ask yourself: what should you do if you discover that a security gap has not been closed? The practical answer is to set a deadline, make one upgrade, and confirm it worked—don’t let it linger as a “later” project.

What To Do Instead

- Pick a safe with a clearly stated fire rating and a sealed design intended to reduce water intrusion.

- Store cash in an envelope or cash band inside the safe, not loose (it reduces tearing and miscounts).

- Keep an inventory note outside the safe (not listing the amount) so you remember what belongs there.

Mistake 3: Treating Home Cash Like Your Whole Emergency Plan

Home cash helps during outages and short disruptions—but relying on it for the entire emergency fund can create new problems: temptation spending, under-saving, and missing fraud protections you get with regulated accounts. This is also where behavior matters. If you’ve ever asked, how much more do you spend on purchases when you use credit instead of cash, many people notice they spend more with credit because it doesn’t feel as immediate—yet cash at home can also disappear through “small” withdrawals that add up.

A balanced plan separates “immediate cash” from “stable reserves.” That’s often the real answer to where to put extra money and the best place to put extra money: keep only a limited amount of bills at home, and keep the rest somewhere safer and easier to track.

A Simple Split That Stays Practical

| Need | Storage Approach | Why It Helps |

|---|---|---|

| Same-day essentials | Small home cash reserve in a fire-rated safe | Access during outages without overexposing your full fund |

| Short-term emergencies | Insured bank or credit union savings | Better protection, tracking, and fewer loss scenarios |

| Longer-term reserves | Separate high-yield savings or Treasury-focused options | Liquidity with potential interest, without keeping paper cash at risk |

Budget And Payment Choices That Keep Your Emergency Cash Intact

Emergency cash disappears fastest when there’s no plan for day-to-day spending. One reason to create a budget is to know what you can and can’t afford—so your at-home reserve stays for emergencies, not convenience. Also consider your payment habits: the use of a debit card to purchase an item or service at a retail store can help you avoid carrying large cash amounts while still keeping spending connected to real balances.

Quick Credit Safety Tie-In For Financial Resilience

Securing an emergency fund also means reducing the chance you’ll need it because of identity theft. If you’re reviewing your protections, which of these laws gives you the right to know what is in your credit file is the Fair Credit Reporting Act (FCRA), which supports your right to access and dispute information in your credit reports.

FAQ

Where Should You Keep Large Amount Of Money At Home?

If you must keep a larger amount briefly, use a fire-rated safe that can be anchored, and avoid obvious rooms and “common hiding places.” For most households, limiting the amount stored at home reduces risk more than any clever hiding method.

What Is The Safest Place To Put Money For Emergencies?

A small amount of cash at home can be useful, but for the bulk of an emergency fund, insured deposit accounts are typically safer than paper cash. This approach also helps with tracking and reduces loss from fire or theft.

When Would It Be A Good Investment To Sell Bonds At A Discount From Par?

It can make sense when interest rates have risen and you want to reinvest into higher yields, when you need liquidity for a true emergency, or when tax planning makes realizing a loss useful. The right move depends on your timeline and overall plan—not on trying to “win back” a discount quickly.

What May Occur If You Do Not Include The Scope Of The Ra When Defining It?

In a risk assessment, an unclear scope can lead to missed threats (like fire or unauthorized access), wasted effort on low-priority issues, and a false sense of security. Defining scope keeps your home cash plan focused on the risks that actually matter.

Conclusion

To secure your emergency fund at home, avoid these three mistakes: using obvious hiding spots, skipping fire/water protection, and relying on home cash as the whole plan. A small, protected cash reserve paired with safer off-site savings can keep emergencies manageable without turning your home into a single point of failure.

Disclaimer: The information provided in this article is for educational and informational purposes only. It does not constitute professional advice. Readers should conduct their own research and consult with qualified professionals before making any decisions.