Rent to Own RV Options: How to Find Affordable Deals

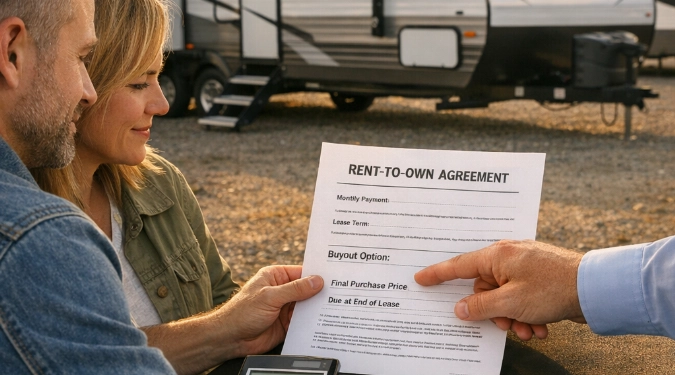

Rent to own RV options can be affordable—but only when you understand how the contract converts payments into ownership and what costs hide behind a low monthly number. This guide breaks down the most common rent-to-own structures (dealer lease-purchase, private-party arrangements, consignment payment plans, and financing comparisons), the specific deal terms that control total cost, and a step-by-step method to price-check, inspect, and confirm a realistic buyout. You’ll also learn how “no credit check” or “no deposit” claims may change the total paid, what to verify when bad credit or zero-down offers are advertised, and which questions protect you from fees, repair surprises, and hard-to-exit agreements.

Rent-to-own RV options can feel like the bridge between “not ready to buy” and “tired of renting.” The key is finding a payment structure you can actually sustain, spotting true low-cost paths (not just low monthly ads), and knowing which questions uncover hidden costs before you commit.

What Rent-To-Own Really Means For An RV

In a rent-to-own setup, you typically make regular payments to use the RV now, with the intention of owning it later. Some programs credit part of each payment toward purchase, while others treat payments as rent until you exercise a purchase option. Because structures vary, affordability depends on the contract details more than the headline payment.

Many shoppers are drawn to rent-to-own RVs marketed as having no credit checks or deposits. Those offers exist, but the tradeoff is often a higher total paid over time, stricter rules for damage, or limited RV selection. Reading the “how ownership happens” section of any agreement is where affordable deals are either confirmed—or ruled out.

The Main Rent-To-Own RV Options That Can Be Affordable

Lease-Purchase From An RV Dealer

A dealer may structure a lease with an option to buy later. This can be affordable when the buyout price is clearly defined and you’re not paying inflated fees. Ask whether any portion of monthly payments reduces the buyout and how mileage, wear, and maintenance are handled.

Owner-Financed Or Rent-To-Own From A Private Party

Private sellers sometimes offer rent-to-own terms, especially for older travel trailers and Class C rigs. Affordability improves when you can negotiate a realistic purchase price and a short trial period. Protect yourself by documenting the condition, who carries insurance, and what happens if either side ends the agreement early.

Consignment Lots And “Payment Plan” Arrangements

Some consignment dealers facilitate payment plans where the RV stays on the lot until you’ve paid enough to take delivery. This can reduce risk, but it’s only an “affordable deal” if the fees are transparent and the RV’s price matches comparable listings.

Traditional Financing As The Alternative Benchmark

Sometimes the most affordable “rent-to-own” move is realizing you don’t need rent-to-own at all. Comparing the full rent-to-own total against purchase financing (including taxes, insurance, and expected repairs) helps you avoid overpaying for convenience. You may see ads for RV Financing with no Down Payment, which can be real in some cases, but approval depends on lender rules and the RV’s age and value.

What Makes A Rent-To-Own Deal Truly Affordable

Affordability is about total cost and risk, not just the monthly number. A deal can be considered lower-cost when the RV’s sale price is close to market value, fees are limited, the path to ownership is explicit, and you can exit without losing an extreme amount of money.

| Cost Factor | What To Look For | Red Flag |

|---|---|---|

| Purchase Price | Matches similar year/model/condition listings | Marked up “because it’s rent-to-own” |

| Payment Credit | Clear amount credited toward buyout | No credit, or vague language |

| Fees | Itemized, limited, and explained | Stacked admin, inspection, or “program” fees |

| Maintenance | Who pays for tires, roof, brakes is specified | You pay everything but don’t build equity |

| Exit Terms | Reasonable early-return terms | Large penalties that trap you |

How To Find Affordable Rent-To-Own RV Deals Step By Step

Use a process that forces clarity before emotion takes over:

- Pick your “must-fit” RV type and age range (travel trailer vs fifth wheel vs Class C) so you can price-check accurately.

- Build a total monthly budget that includes insurance, storage, campground nights, and a repair cushion.

- Price-check the exact model across multiple listings to confirm the rent-to-own price is not inflated.

- Ask for the full contract terms in writing before any money changes hands.

- Get an independent inspection when possible, especially for water intrusion, roof condition, slide-outs, and appliances.

- Compare the rent-to-own total paid versus a financed purchase scenario.

Bad Credit And Zero-Down: What To Know Without Getting Trapped

Some shoppers specifically look for Zero Down Rv Financing because cash is tight up front. That can reduce the barrier to entry, but it may also increase the total cost through higher rates or stricter lender requirements. If you see Zero Down Rv Financing Bad Credit offers, confirm what “bad credit” means to that lender and whether income, RV age, or loan term changes the deal.

Be cautious with ads that imply instant outcomes. Phrases like Rv Financing Instant Approval can simply mean a quick prequalification step, not final approval or final pricing. Also, marketing language such as Guaranteed Rv Financing Near Me is often just advertising phrasing—treat it as a prompt to verify lender criteria, not a promise.

If you’re searching for Bad Credit Rv Dealers Near Me, focus on dealers that provide full itemized pricing, allow inspections, and clearly disclose whether the RV is sold “as-is.” That transparency is often the difference between an affordable path and a costly surprise.

FAQ

Can Rent-To-Own RVs Really Have No Credit Checks Or Deposits?

Some programs may not run traditional credit checks or may offer low-to-no deposit entry, but they often offset risk through higher payments, tighter rules, or higher total cost. Ask what happens if you return the RV early and whether any payments apply toward ownership.

Do Monthly Payments Build Ownership Automatically?

Not always. Some agreements credit a defined portion toward a buyout, while others are pure rental until you choose to purchase. Affordable deals make the credit amount and buyout price unmistakably clear.

Who Pays For Repairs In A Rent-To-Own Agreement?

It varies widely. Many contracts place routine maintenance on the renter, while major failures can be disputed if the contract is vague. A strong agreement spells out responsibility for tires, brakes, roof leaks, appliances, and slide-out service.

What Should I Inspect Before Agreeing To Rent-To-Own?

Prioritize water damage (roof, walls, around windows), electrical and propane systems, holding tanks, tires (age and wear), and the operation of slide-outs and leveling systems. These items can turn a seemingly affordable deal into a high-cost commitment.

Conclusion

Rent to own RV options can be a practical way to reach ownership with a smarter payment structure—especially when you verify the real purchase price, fees, repair responsibilities, and exit terms. The most affordable deals are the ones where the total cost is transparent and the path to owning the RV is clearly written, not implied.

Disclaimer: The information provided in this article is for educational and informational purposes only. It does not constitute professional advice. Readers should conduct their own research and consult with qualified professionals before making any decisions.